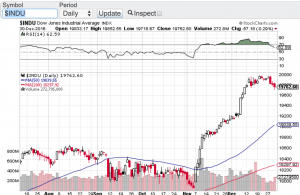

There has been plenty of chatter over the past month or so as to whether or not the Dow Jones Industrial Average (chart) would surpass the 20,000 mark and what that would mean for the markets going forward. Well lo and behold, it did it! For the first time in its history, the Dow Jones Industrial Average (chart) breached the 20,000 milestone mark last week thanks in part to earnings reporting season. The Nasdaq (chart) also continues to set record highs although this week this particular index has recently been challenged by Donald Trump’s commitment to altering the H-1B visa rules which in turn could effect the tech industry in a meaningful way. The S&P 500 (chart) also remains near its all-time highs while the small-cap Russell 2000 (chart) is hovering around its 50-day moving average.

While earnings reporting season remains a key focus for investors, one cannot ignore the constant daily flow of news out of Washington D.C. President Donald Trump like no other has signed double digit executive orders in his first week of office alone fulfilling part of his campaign pledges. These executive orders range from loosening regulations in a variety of industries, to border security, to withdrawing the United States from the Trans-Pacific Partnership Negotiations agreement and to the construction of the Keystone XL pipeline, just to name a few. Without question Donald Trump means business and is acting swiftly about it. We know how the American public feels about this and most recently how corporate America is beginning to speak out, and it’s a mixed bag to say the least.

The question now is how will the markets ultimately react to the new norm, the protectionism posture of the new administration and the swift policy changes that are occurring? Well for the first time in a while market volatility (see chart below) has spiked as investors and traders alike try to digest the ultimate outcomes of such dramatic changes. In my humble opinion, vol is just getting started. Good luck to all 🙂

~George